Offering instant ACH payments means that your clients will have access to their payments as soon as possible and avoid waiting for days for standard ACH payments to process through the clearing house.

When looking for payment solutions, it's essential to consider how quickly and cost-effectively they can be set up. There are several things that you need to think about—these include transaction fees, deposit speeds, processing times, etc.

If you’re looking for a streamlined P2P payment platform, you can consider a payment-as-a-service system like Sila, which offers same-day and Instant ACH products.

How Instant ACH Works?

Instant ACH is a Sila API (Beta) feature that makes funds available in an end user's wallet near-instantly before funds are received from the ACH debit. Instant ACH is only available to the /issue_sila endpoint, not for /redeem_sila.

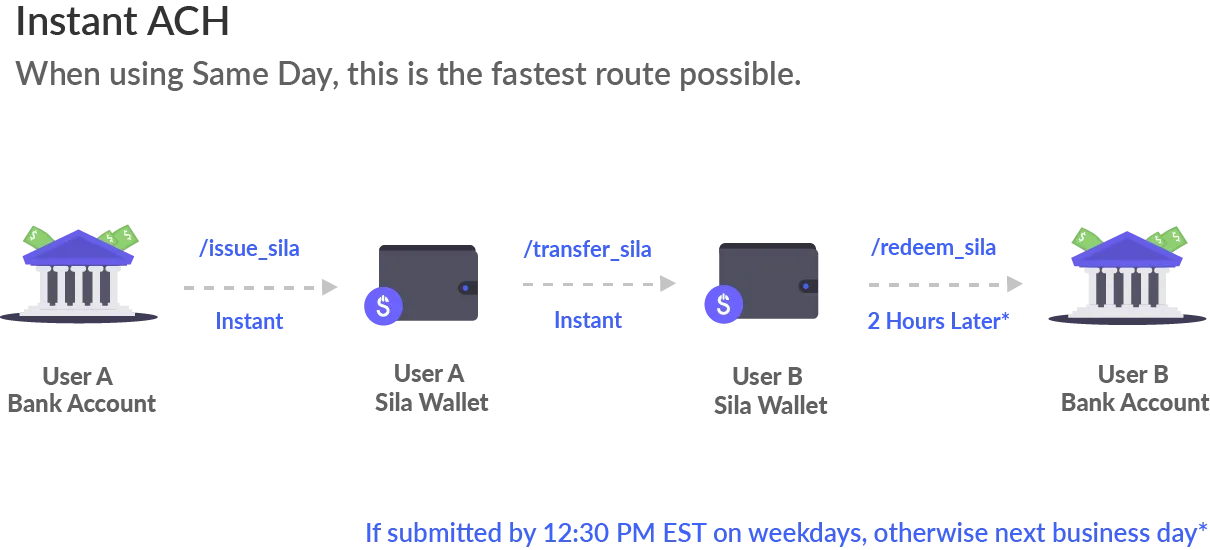

Instant ACH uses Same Day ACH for ACH debits only. Here’s what that looks like:

With the introduction of the ACH’s same-day payment schedule, this makes fast transfers possible. With Sila’s Instant ACH product, you can use faster ACH transfers for your P2P platform.

Offering instant ACH payments can save time and ensure the user can access the funds as soon as possible. Even though the basic ACH payment process is restricted by banking hours, instant ACH payments are available faster for improved customer experience.

As an added security measure, ACH payments for most payment methods also have a dispute, recall, or stop-payment option before the funds are processed.

Understanding Instant ACH Processing Timelines

Instant ACH is a great way to provide speed ACH debit transfers. However, if the transaction is not submitted by 9:30 am PST, it may be delayed by a business day.

To issue, transfer, and redeem the Instant ACH API, the call must occur before the 9:20 am PST cutoff.

Understanding Eligibility and KYC Criteria

One of the most important requirements for sending money through Sila is being compliant with Sila’s KYC (and KYB) requirements. So, to use the instant ACH services, you must comply with the ACH identity verification requirements.

Clients who want to use Sila’s Instant ACH product must use Sila’s full KYC and account linking with the MX Processor Token and that from Plaid.

Maximum Transfer Limits with Instant ACH

There is a default limit for how much you can send through Instant ACH.

However, when you work with your Sila account manager, you could find ways to change that default limit.

Preparing for this maximum transaction amount will improve your customer experience.

Understanding Security and Disputes

Sila's Instant ACH is based on a good funds model, which means that participating banks need to have enough money available at the Federal Reserve when they initiate transactions. Authorized payments with a financial institution cannot be "revoked" or "recalled" once submitted.

Financial institutions can send payments back, even if the receiving bank hasn't processed them. The receiving bank is not obligated to honor the request, however.

The finality of an RTP transaction allows participants to consider a payment complete without having to wait days or hours for the funds to become available. This also means that end users must be vigilant with stringent identity verification.

Instant ACH With Sila

When using Sila’s Instant ACH product, our customers must meet specific criteria to be eligible to provide instant ACH payments; this is enforced to protect your business.

ACH Originator

To be an ACH originator, platforms need to ensure that they meet the following requirements:

- The platform must keep any customer data—including banking information—sent over a secure, encrypted network.

- Banking information should be protected by storing it on-site or using encrypted cloud storage. Data can be stored securely by choosing PCI DSS-approved hardware and software.

- Counterparties to each ACH transfer must be checked against sanctions enforced by the U.S. Treasury’s Office of Foreign Assets Control (OFAC) to ensure the organization or individual isn't assisting any foreign entities or individuals engaged in financial crimes.

- Multi-factor authentication should be required on accounts

- Additionally, all third-party service providers must pass an extensive vetting process to determine their legitimacy

ACH payment processors are guided by many applicable regulations, including those administered under the Electronic Funds Transfer Act (EFT Act).

Bank Account Linking

Secure bank account linking and a process that includes a verified KYC and KYB system is important for Instant ACH and Same Day ACH transfers. That is why Sila users who want to use Instant ACH must use a service like MX or Plaid, and a processor token to link accounts.

Implement Customer Onboarding

Customers will need to complete registration, including enhanced anti-fraud verification and device confirmation via SMS messaging.

- Sila platforms must perform identity verification (full KYC or KYB) on each user

- SMS notifications and confirmation notifications must be enabled confirmations for all instant ACH transactions to process instant ACH

Sila will run a real-time risk assessment on the ACH debit transaction and determine if it is eligible for instant issuance. Sila sends an SMS confirmation for the transaction, and once the end user confirms the message, Sila tokens are instantly issued and available for transfer/redeem.

Trust Instant ACH With Sila

At Sila, we connect you to the ACH Network and secure payment processing. With Sila’s “instant” ACH feature, customers have faster payment options.

Chat now with one of our payment experts to find out how to send and receive money faster for your P2P platform. With built-in safety checks from Sila, your app will be safe and secure. We build the infrastructure; you bring innovation and the customers.

With Instant ACH by Sila, you'll have access to fast payments via instant ACH payments. Allowing for near-instant settlement so that your customers don't have to wait for standard bank business days for transfers. You can give your clients access to their money when they need it and at the speed that is right for both of you.