It’s an exciting time in payments here in the US, but it’s also a confusing and difficult-to-navigate time for many. Let’s talk about why and what Sila’s doing to solve this.

With the launch of FedNOW and the increasing adoption of RTP, we can finally send funds instantly between most bank accounts in the US. We also have options for how to do that – from transferring funds to a friend via Venmo to deciphering how your bank wants you to send that kidnapping payment via Zelle, RTP, or FedNow.

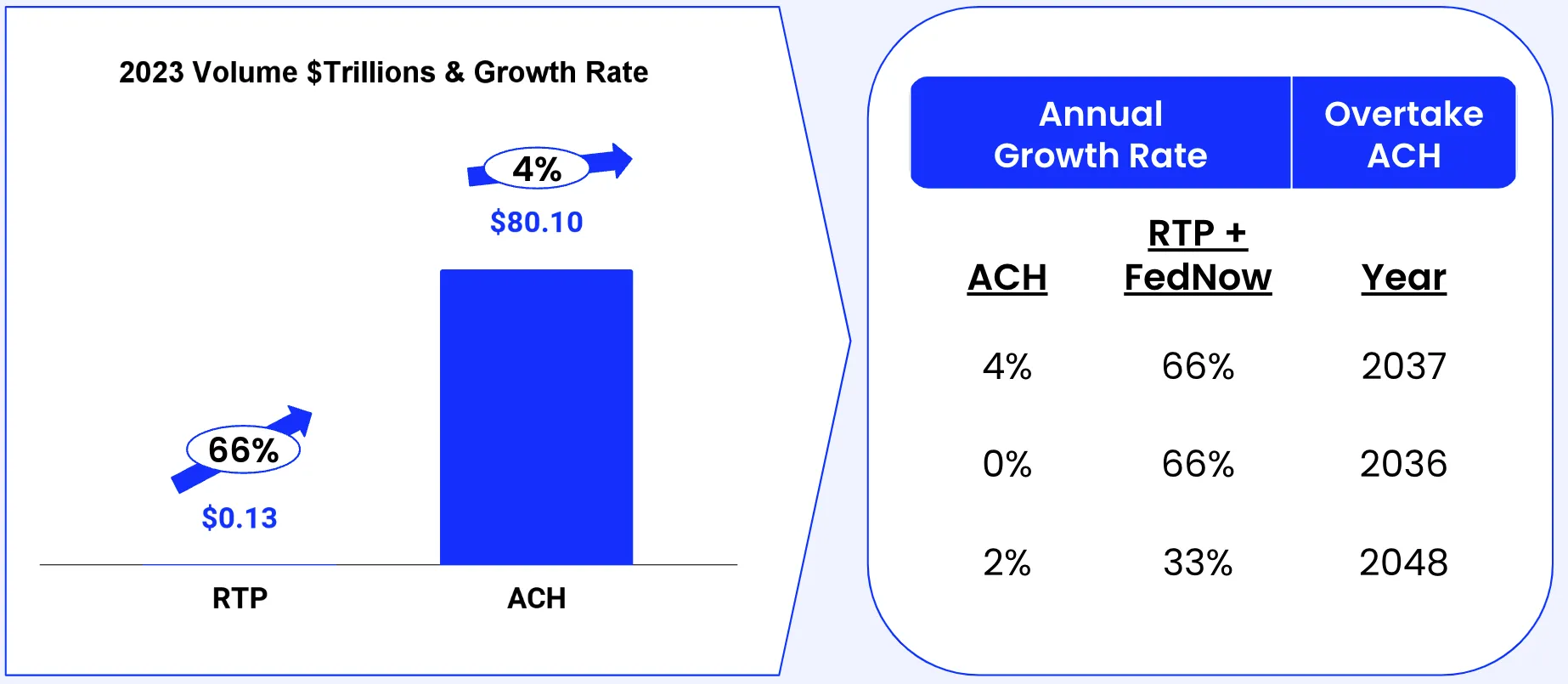

At the same time, ACH still dominates retail payments in the US by volume and transactions, and even with the introduction of RTP and FedNow, ACH continues to grow. ACH is so old that the average Senator remembers its creation during their teenage years. In those decades of use, it has become the country's infrastructure and foundation of finance. At current growth rates, RTP and FedNOW won’t overtake ACH till 2037, and, likely, we will still be sending payments via NACHA files sent over sFTP in 2050.

This puts the entire payments industry in a difficult position: how do we navigate a world where ACH might be in decline but still dominant, where some banks can do some things on RTP, and where the newest entrant, FedNow, has powerful backing, supports a broader set of use cases, but is still far from ubiquitous.

Our customers, prospects, and peers in the industry know that people want to use instant payments but don’t want to build multiple integrations to different payment systems or manage the complex logic to route transactions between systems. Instant might seem significant if you’re an online gaming startup starting with a blank slate, but what about the rest of us?

As a small commercial lender, you’d love to have 60%+ of your disbursements and repayments completed in less than 10 seconds, but you don’t have the budget or the access to engineering talent to invest in this. If you’re a payroll provider for a restaurant, you’d love to have payroll land in a server’s account a few minutes after their shift ends, but you don’t want to be in the business of tracking what payment rails and what employee bank account is accessible on which payment system. Fifty years of ACH means 50 years of legacy implementations that need a bridge to the world of instant payments.

Sila was founded with the intent to combine blockchain and ledgering. Over the past five years, we’ve built deep expertise in the world of ACH and how a seemingly frozen file format in practice contains incredible complexity that we needed to learn to manage. We transitioned from blockchain to our own ledger a while back, but in building our original platform around the ability to offer services on the Ethereum blockchain, we created an orchestration and ledgering platform designed to transact 24/7 and to work across methods and providers to turn ACH transactions into instant ones.

This week, we’ve announced our ACHNow product, where you can plug us into existing ACH infrastructure – including giving us those NACHA files you’re sFTPing now – and we will settle them instantly, choosing the right rail and provider based on your need (you can literally call “--cheapest” “--fastest” or anything between), turning them into instant payments if possible. If not, we use our Instant Settlement product to settle funds to your account immediately.

ACH pulls are a nightmare, as anyone who’s had to implement or use them knows, and with ACHNow, we’ll reduce those problems by attempting them instantly. The percentage of instant transactions will increase dramatically over the next few years as RTP and FedNOW coverage increases. The best thing is that you don’t have to do a thing - as coverage increases, your instant % will increase without rewriting a single line of code.

You don’t have to make a choice and bet on RTP or FedNow or build both on top of your ACH. We make the best choice based on availability and your own needs for that transaction. You keep using ACH and get ~40% of your transactions on the instant rails today, and 100% of them settle instantly. Then, over time, as the adoption of instant rails increases, clients benefit without needing to do any further work. Sit back and enjoy the long ascent of instant payments while you delight your customers.

Sila has taken very complex systems and designed a simple/elegant solution. You don’t have to manage reserve account requirements at two, three, or four banks. We’re managing the ledgers, we’re handling the float between banks, we’re negotiating the lines of credit to bridge the time and liquidity gaps, and we’re finding the right partners so you don’t get into shouting matches with a harried New Jersey bank compliance person about whether you’re a third-party nested payment provider that needs a set of Money Transfer Licenses.

It’s the culmination of my vision of helping customers by making the complicated simple so they can concentrate on their business. I’m so proud of ACHNow and for being here to help.

I’d love to talk more about the future of payments and Sila’s willingness to help with adoptions – I’m at Fintech Meetup next week, or please, you can email me your thoughts or comments at shamir [at] silamoney [dot] com

Shamir Karkal, Co-founder and CSO at Sila