Sila’s payment processing technology gives fintech innovators more options to explore and expand financial futures. Luckily with a product like Sila, you don’t have to change a business idea too much to fit a certain mold. But with so many financial vendors to choose from and features throughout, it can be a challenge to find a financial platform that fits your business idea.

You may search for the right financial vendor and get caught up with these comparisons. Know that Sila is more than a payment vendor. In reality, we offer banking infrastructure and the ability for your business to create your own financial features in your business.

To help you understand our offerings, we’ve written this article comparing infrastructure vendor Dwolla with our services. Read on to learn more:

What Does a Banking Infrastructure Platform Do?

Banking infrastructure platforms are fintech software solutions that enable payment platforms to be built, allowing money transfers features for businesses. These platforms can come in the form of an API, website, or SaaS integration (like an API endpoint) which can be integrated into the business’ user interface and so that users can easily send money directly through the business.

Modern banking infrastructure platforms are sometimes confused with payment infrastructure. However, in reality the two platform types differ. Banking infrastructure platforms will facilitate things like a bank account, digital wallet, and FDIC insurance whereas payment infrastructure will facilitate access to the credit card network and sometimes the ACH transfer network.

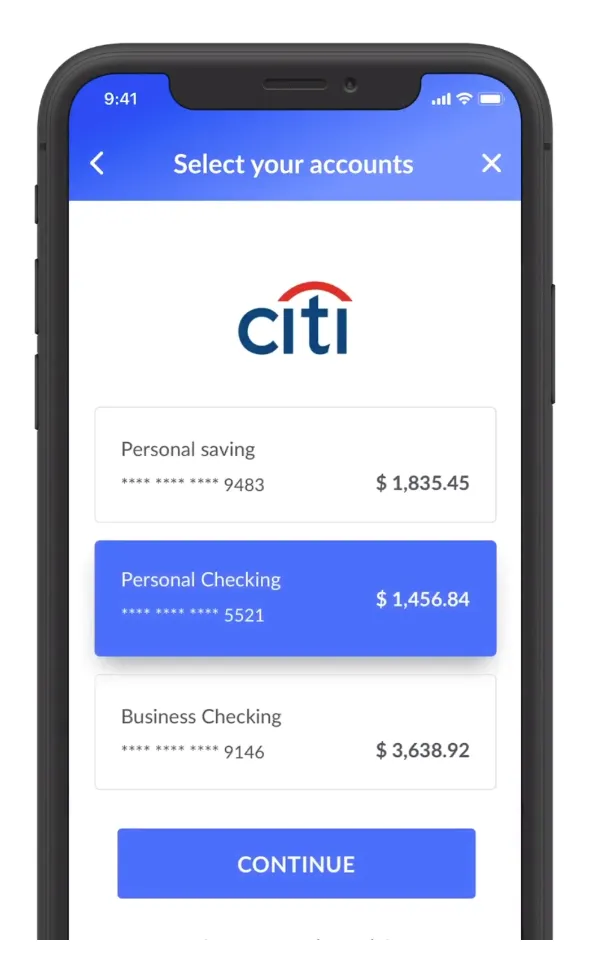

In most cases, both banking and payment infrastructure platforms facilitate bank account linking, identity verification, and money sending capabilities, features that might be used in business-to-client banking for ease of use, compatibility, and functionality.

Common payments platforms like Square, Stripe, Plaid, PayPal, Moneris, and Venmo exist, in some part, with a banking infrastructure supporting them. And some of these services even help each other when it comes to offloading a lot of the compliance, costs, and time spent building payment apps.

There are distinct differences between payments infrastructure and banking infrastructure. Dwolla facilitates both. Let’s dive into who Dwolla and Sila are so we can better understand this product:

What Does Dwolla Provide?

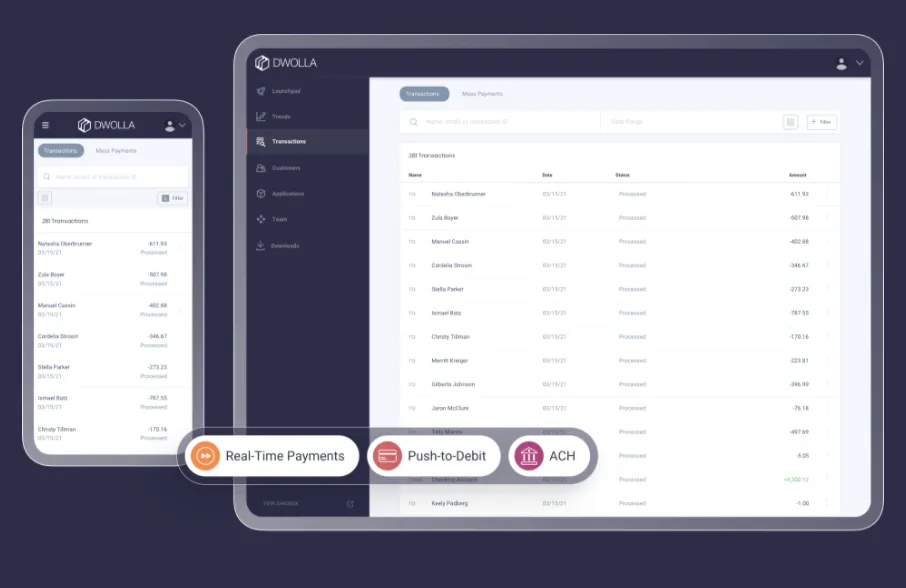

Dwolla is a modern payments platform that allows innovators, like you, to program payments and scale payment features with their technology. With their API code, you can easily integrate money moving programs so that you can facilitate peer-to-peer transfers, bill pay, bank account linking, and more.

Dwolla is essentially a digital payment application. And by partnering with Dwolla for your business, you can reap the benefits of their features as well as offloaded compliance. For example, Dwolla might store data on your behalf in PCI DSS compliance hardware so you don’t have to.

The Dwolla API is incredibly configurable, scalable, and developer-friendly. Dwolla features include:

- The ability to work with banks and credit unions for broad connectivity in the U.S.

- White-label experience

- Configurable API

- Scalable infrastructure

- Tokenization (or the ability to send transactions using unique identifiers to limit sending sensitive data)

- The ability to send, receive, and facilitate total control over the flow of funds

- ACH transfers, including Standard ACH, Next-day ACH, and Same day ACH

- Balance-to-balance transfers

- Push-to-debit

- Real-time payments

- Wire transfers

- Identity verification

- And ledger account management features

- Among others

How Does Sila Support Businesses?

Much like Dwolla, Sila is a payment platform that businesses can integrate into their existing business or new business idea to facilitate funds flows.

Sila’s primary product includes:

- An ACH API

- A wallet API

- Secure bank account linking

- Identity verification

From here, users can scale up as much as they like. As a bank agent themselves, Sila’s users can tap into their security and ledger access through Sila’s partner Evolve Trust.

Personally identifiable information in the customer data is also offloaded through partners including Plaid for bank account linking and Alloy for identity verification. So while clients still need to handle best practices for compliance, by choosing Sila, you are automatically one step ahead of the competition. You don’t need to worry about managing that data and can trust in Sila’s connected partners, or fintech marketplace as we call it.

With Sila, you have a team of partners ready to support your next big idea. And with our status as a bank agent, this will save your company time, money, and lots of setup for getting compliant in complicated financial markets.

Dwolla vs. Sila

When choosing Sila vs. Dwolla, you’ll want to understand your options and future ideas. Sila is the best choice for when you know you’ll eventually want to do things like card issuance, sending international money transfers (through digital wallets), and automating money movement through smart contract technology.

With our patented SILAUSD stablecoin alternative, pegged to the U.S. penny, users can bring their own smart contract technology and issue secure, FDIC-insured tokens along ER-20.

You really don’t get this level of scalability with Dwolla.

Dwolla might be white-label, customizable, and integrate with your current systems (just like Sila is), but there is a lot more work that goes into this relationship. With Sila, you don’t need to worry as much about risky users using your products, because all Sila clients have KYC/KYB included. Additionally, data storage best practices are used no matter what, through our partnerships, so there is less stress and money spent in this regard.

With lower fees and more versatility, Sila users are finding that they are able to create something they didn’t even know was possible.

Sure, if you want to be the next Venmo, then you need a banking partner. But what if you want to apply smart contract technology to agreed-upon services? Here’s where Sila steps in.

Choose Sila to Grow While You Do

In all honesty, going with Sila is a smart choice. Our dedicated customer success team, strong compliance leadership, and powerful technology will ensure that you experience fewer hiccups along your path to success.

If you have questions, reach out to anyone here at the Sila team. You can always check out our product demo every Thursday, check out our Youtube or head over to our sandbox to test the product yourself!